Market Thoughts

When is the last time we had Rate cuts and QE at the same time?! We just got both and although it may not time or rhyme with 1995 and 1998 or 2001 and 2007, it certainly does feel foreboding given both trade tensions AND economic slowdown.

THAT was my opening sentence for this Daily Market Thought before Trump’s tweet this afternoon which brought the market down hard.

I was getting lunch and about to go outside and get some sun when I got a double SMS trade alert on my GS short – both partial and full positions were closed so both price targets I had set had triggered. Odd I thought. I had JUST tweeted banks were fading. Then I looked and saw GS wasn’t down over 2.5% because the debt ceiling bill passed – although that was The Tell for me market was weakening as I had been watching for all day. The real push lower was Trump threatening the next traunch of tariffs on China for Sept 1st.

BREAKING: Trump Ratchets Up Trade War. Threatens To Tariff All Chinese Goods on Sept. 1. Bloomberg

And with that, the market TURNED hard and my morning market call that ES would see $2958 came true and then some. I did NOT have on enough shorts… I did NOT take off but half of my gold/silver/miner shorts this AM… I did NOT position aggressively with volatility as I expected. I should have anticipated Trump would pull this SO SOON post Fed, with whom he is not pleased, and because it IS the ‘known’ risk in this market environment. Otherwise, we could have had an opportunity for a quiet August after NFP tomorrow and after Big Tech having reported and Big Economic indicators not due up until same time as Jackson Hole Aug 22-24.

Literally, I just wrote for clients this week: My Volatility Watch May Be One In The Same With My Recession Watch. It is scheduled for posting Friday at noon.

Anyway, Trump/Tariff Man tweeted and I went back to my computer and entered some SMH + BA shorts. I was surprised MSFT did not fall more but then Trump has asked DOJ to look into AMZN as contender for JEDI contract and MSFT stayed green (it is their contract to lose it appears, and a sizable one at that at $10B.). Clients will notice that my (newly entered) IWM + (partial) Oil longs were stopped out. Luckily, my ‘bottom fishing plays” recently entered weren’t hit hard and I had closed all 3 positions long in K post EPS for Big Wins this morning. Despite the sudden drop, my portfolios are doing quite well:

Risk Happens Fast.

I was doubting my morning call when I went to lunch…

@WallStreetJane Aug. 1st, 9:15 am Samantha Says: See /ES heading to 2958 today

SPY Trump tweets spur highest option volume day of the year. Total option volume just under 28M contracts today is a 2019 record, and the busiest day since December 21st when over 31M contracts changed hands @OptionAlert

BROKERAGE-TRIGGERED TRADE ALERTS!

China’s Potential Impact on Our Markets

From a colleague to ‘size’ the risk to US equities if China retaliates:

Chinese Tsy owns about $3.4Tn USD assets. plus $1.5Tn USD loans via (1belt-1road initiative etc). and the 3.4Tn is mostly bond ,only 200-250Bn US Equity.There is also about $1.6-1.9Tn USD Corporate debt issued in the US, using Chinese assets as collateral, mostly via Caymen shell companies. Defaulting on those would be ugly

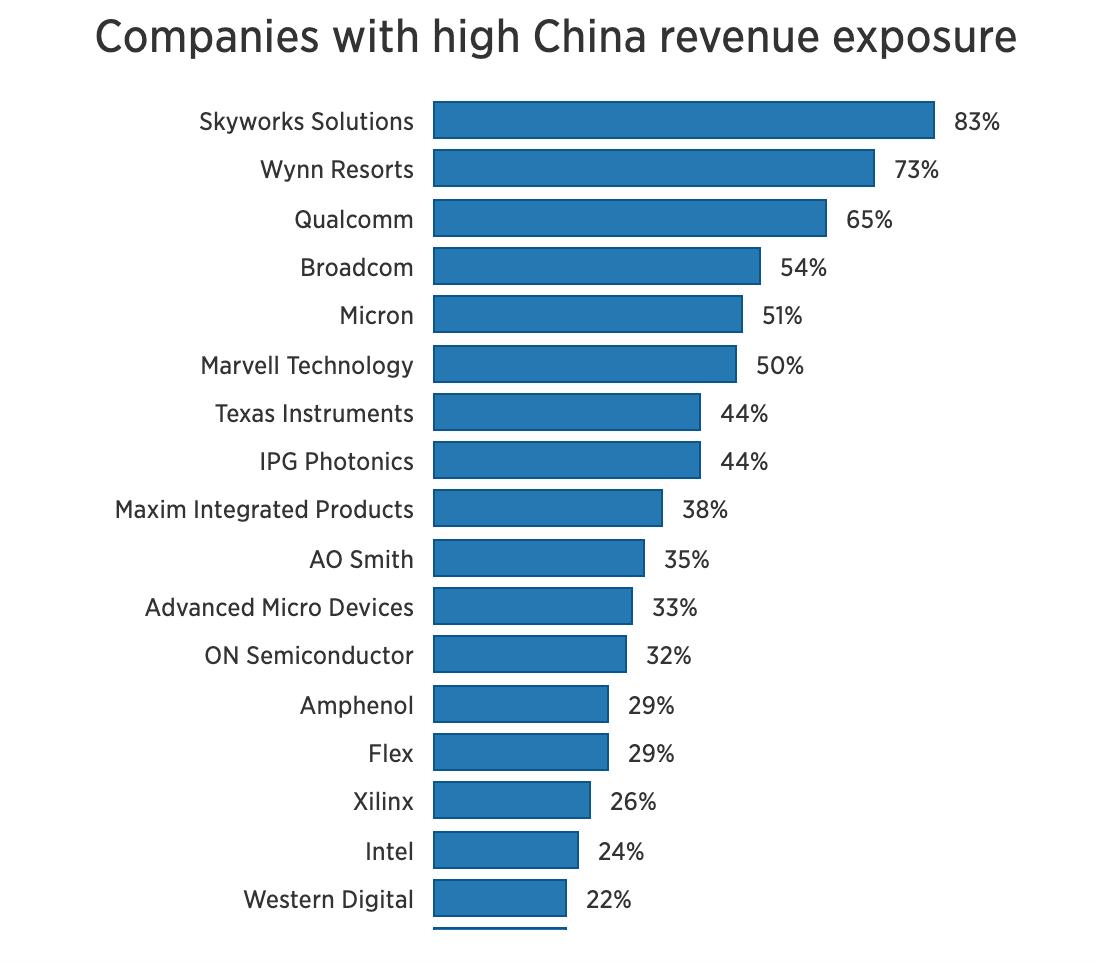

I think this is an excellent time to resend this list of US Companies with high China revenue exposure:

“The reality is that the game is reality versus perceptions. And when the perceptions are worse than the future reality markets rise. When the future reality is worse than the perception, markets fall.” Ken Fisher

Samantha Says

Market Commentary from Samantha’s Live Trading Room and StockTwits Premium Chat Room

Aug. 1st, 9:15 am See /ES heading to 2958 today

Aug. 1st, 9:12 am Market Thoughts: From QT to QE in a New York Minute https://laductrading.com/2019/market-thoughts-from-qt-to-qe-in-a-new-york-minute/

Aug. 1st, 11:09 am Also looking at CAG for a long position.

Aug. 1st, 3:07 pm Hey, I was getting lunch and about to go outside and get my tan on when I got a double SMS trade alert on my GS short. I had JUST tweeted banks were fading but geeze! Then I saw it wasn’t the debt ceiling passing – although that was The Tell for me – it was Trump threatening the 2nd traunch of tariffs on China for Sept 1st. And with that, the market TURNED and my AM prediction that ES would see $2958 came true and then some. I did NOT have on enough shorts… I did NOT take off all of my gold/silver/miner shorts this AM… I did NOT have an idea Trump would pull this SO SOON although that IS the risk in THIS market. Otherwise, we could have had a quiet August after NFP tomorrow with Big Tech having reported and Big Economic indicators not due up until same time as Jackson Hole Aug 22-24. So Trump/Tariff Man strikes again and I ran back to my computer and entered SMH + BA shorts and that’s all that filled at same time my IWM + USO longs were stopped out. Market A Mess – Not Done

Wall Street Jane’s Journal

Jane is not only Samantha’s Live Trading Room moderator, she facilitates client engagement and relays Samantha’s trade ideas into the LaDucTrading StockTwits Premium Room. A former banking VP during the GFC, she now trades full-time and actively shares her trading ideas, plan and process.

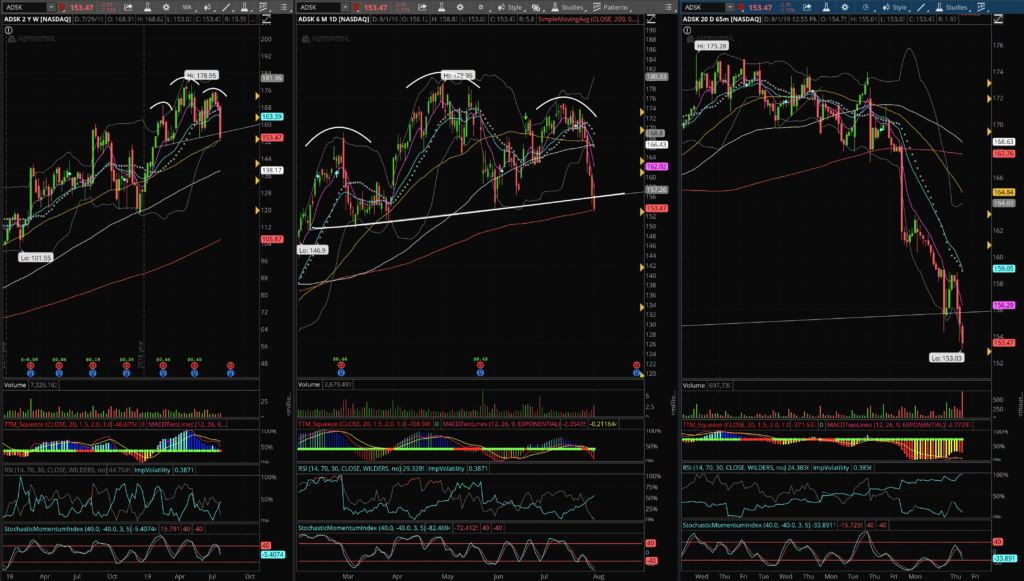

Follow Up: $ADSK

Last night I talked about $ADSK and the head and shoulders pattern that it was at decision point. Today it broke and closed below the neckline. It was green up until the Trump tariff tweet. It closed the day right at major support of the 50WK and 200D moving averages. I didn’t trade this in part because the IV is so high and it’s oversold on shorter timeframes. Will be watching to see what happens over the next few days and weeks.

Macro Matters

Economic Data

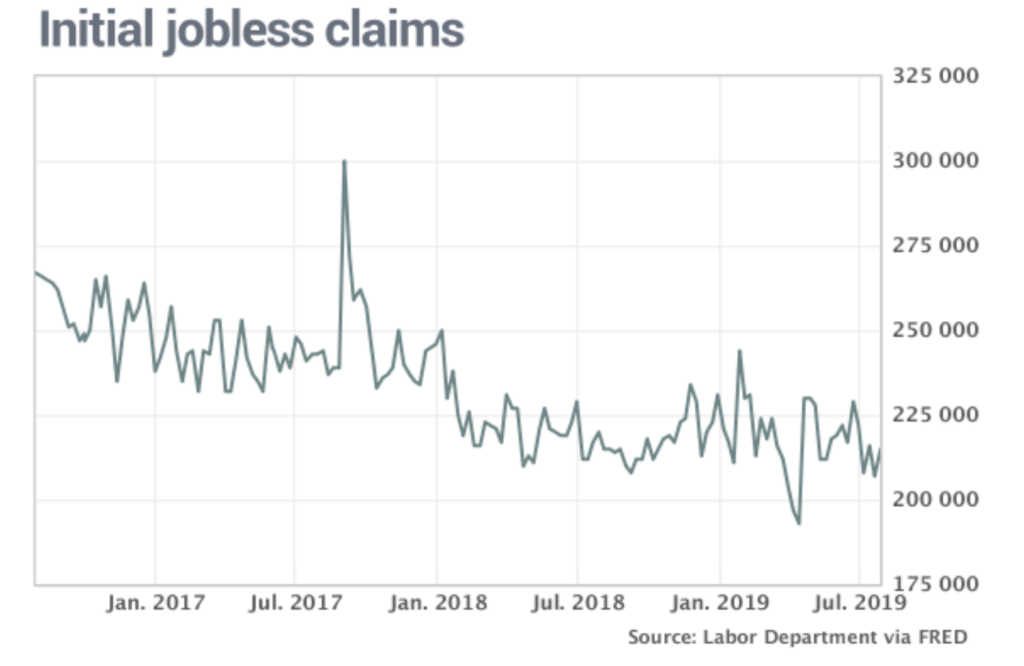

Weekly Jobless Claims: Initial jobless claims rose by 8,000 to 215,000 in the seven days ended July 27

More workers applied for unemployment benefits at the end of July, but the rate of layoffs in the U.S. clung near the lowest level in decades and showed no sign of rising.

Initial jobless claims rose by 8,000 to 215,000 in the seven days ended July 27, the government said Thursday. Economists estimated new claims would total a seasonally adjusted 210,000.

ISM Manufacturing Index: ISM manufacturing index drops to 51.2% in July

American manufacturers grew in July at the slowest pace in three years thanks to festering U.S. trade disputes that have hurt exports and undermined the global economy.

The Institute for Supply Management said its manufacturing index slipped to 51.2% last month from 51.7% in June. That’s the lowest reading since August 2016.

New orders rose a bit faster, but they aren’t growing much. The new-orders index edged up to 50.8% last month from 50%.

Construction Spending: Construction spending dropped 1.3% in June, the biggest decline in seven months, after falling 0.5% in May.

Senate Clears Two-Year Debt, Budget Plan for Trump’s Signature

The Senate sent President Donald Trump legislation to extend the debt limit and allow more government spending until after next year’s election — a bipartisan deal that drew opposition from some who expressed concern about the deficit.

Trump backs the plan, which passed 67-28 on Thursday. The House voted 284-149 for the measure last week with most Republicans in opposition even though the president had urged them to support it.

The measure suspends the debt limit through July 31, 2021, eliminating the risk of a default until then. It also sets budget caps for two years that will permit $324 billion in additional domestic and defense spending above the current cap levels.

Trade Wars and More

China sees intensive contact ahead of next trade talks; small U.S. soybean sales reported

U.S. and Chinese negotiating teams will be in intensive contact to prepare “good groundwork” for trade talks in September, the commerce ministry said on Thursday, as Washington confirmed China’s first private purchase of soybeans since a tariff war broke out more than a year ago.

Talks between the two sides broke down in May after U.S. officials accused China of pulling back from earlier commitments. Washington sharply hiked tariffs on $200 billion worth of Chinese goods and Beijing retaliated, escalating the trade dispute.

“With regards to this (week’s) round of negotiations, both sides communicated over two topics: One is how we view the past – we mainly discussed why negotiations broke down and clarified our views on some economic and trade issues,” commerce ministry spokesman Gao Feng told reporters at a regular briefing.

“The other one is how we view the future to ascertain the principles and methodology of negotiations, as well as relevant timetables.”

South Korea-Japan talks falter ahead of decision on favored-trade list

South Korea called on Thursday for Japan to allow more time for diplomacy as talks on their most serious dispute in years failed to make progress, a day before Japan could remove South Korea from its list of favored trade partners.

South Korea warned that if Japan were to drop it from its so-called white list of countries that enjoy minimum trade restrictions, there could be sweeping repercussions, including damage to bilateral security cooperation.

Markets Confounded by BOE Brushing Aside Risk of No-Deal Brexit

The U.K. central bank’s refusal to acknowledge the risk of a no-deal Brexit, which has driven the pound to a 2 1/2-year low, has disappointed investors who expected the institution to bring some clarity to the matter.

The pound has tumbled since Boris Johnson took over from Theresa May as Prime Minister last month as traders price in a bigger chance of Britain leaving the EU without an agreement on Oct. 31. At the same time, central banks across the world are signaling looser monetary policy, with the Federal Reserve delivering a quarter-point rate cut Wednesday.

Sterling dropped as much as 0.7% to $1.2080, the lowest level since January 2017, before paring losses to trade above $1.2100. Ten-year gilt yields dropped two basis points to 0.59%, the lowest level in nearly three years.

Great Reads

This would be life changing for so many people: A solar-powered system can turn salt water into fresh drinking water for 25,000 people per day. It could help address the world’s looming water crisis.